USA In-Vitro Diagnostics Market Size and Forecast 2026–2034

Rising Demand for Early Disease Detection and Advanced Diagnostic Technologies Driving Growth Across the United States

Introduction

The United States In-Vitro Diagnostics (IVD) market is poised for steady growth during the forecast period as healthcare systems increasingly rely on advanced diagnostic technologies for early disease detection and effective treatment monitoring. The rising burden of chronic and infectious diseases, combined with technological innovations in diagnostic testing, is significantly driving market expansion.

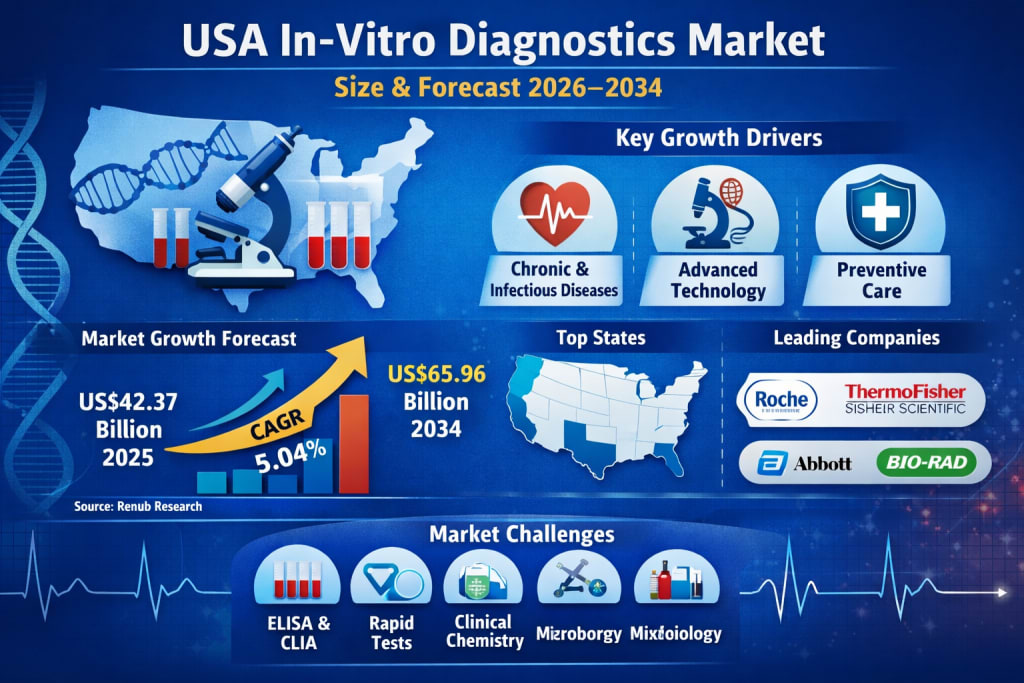

According to Renub Research, the United States IVD market is expected to grow from US$ 42.37 Billion in 2025 to US$ 65.96 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 5.04% from 2026 to 2034. This growth reflects the critical role diagnostic testing plays in modern healthcare systems, especially in preventive care and personalized medicine.

In-vitro diagnostics refers to medical tests performed on biological samples such as blood, urine, saliva, or tissue extracted from the human body. These tests help detect diseases, monitor health conditions, guide treatment decisions, and support wellness management. IVD technologies include diagnostic instruments, reagents, test kits, and software systems used across clinical chemistry, immunoassays, molecular diagnostics, hematology, and microbiology.

The United States continues to lead the global IVD industry due to its advanced healthcare infrastructure, strong research ecosystem, and high adoption of innovative diagnostic technologies.

United States IVD Market Overview

In-vitro diagnostics have become an essential component of the modern healthcare ecosystem. They provide physicians with accurate information needed to diagnose diseases, monitor therapy responses, and assess patient health outcomes.

The United States represents one of the most mature and technologically advanced diagnostic markets in the world. Hospitals, diagnostic laboratories, and research institutions across the country are rapidly integrating cutting-edge diagnostic technologies such as molecular diagnostics, next-generation sequencing, artificial intelligence-enabled diagnostics, and point-of-care testing systems.

Several factors contribute to the strong demand for diagnostic services in the United States:

High prevalence of chronic diseases such as diabetes, cancer, and cardiovascular disorders

Growing aging population requiring regular diagnostic monitoring

Increasing adoption of preventive healthcare screening programs

Favorable reimbursement policies supporting diagnostic testing

Rapid advancements in biotechnology and molecular testing technologies

Additionally, the growing focus on precision medicine has further strengthened the role of diagnostics in healthcare decision-making. Genetic testing and biomarker-based diagnostics are increasingly being used to tailor treatments according to individual patient profiles.

Key Growth Drivers of the United States In-Vitro Diagnostics Market

Rising Burden of Chronic and Infectious Diseases

Chronic diseases remain the leading cause of death in the United States and represent a major driver of diagnostic testing demand. Conditions such as diabetes, cardiovascular diseases, cancer, autoimmune disorders, and hypertension require continuous monitoring and early detection through laboratory tests.

According to the U.S. Department of Health and Human Services, approximately 129 million Americans live with at least one major chronic disease. Furthermore:

42% of Americans have two or more chronic conditions

12% live with at least five chronic illnesses

These conditions require regular diagnostic testing to manage disease progression and monitor treatment effectiveness.

Chronic diseases also place a significant financial burden on the healthcare system. Nearly 90% of the US$ 4.1 trillion spent annually on healthcare in the United States goes toward managing chronic diseases and mental health conditions.

In addition to chronic illnesses, periodic outbreaks of infectious diseases increase the demand for diagnostic testing. Rapid identification of pathogens and disease monitoring through diagnostic tests plays a critical role in public health management.

The increasing elderly population further amplifies demand for diagnostic services, as older individuals often require more frequent health screenings and medical monitoring.

Advanced Healthcare Infrastructure and Technological Leadership

The United States benefits from one of the most advanced healthcare infrastructures globally, enabling rapid adoption of new diagnostic technologies.

Hospitals, academic medical centers, diagnostic laboratories, and research institutes are continuously investing in innovative diagnostic tools such as:

Molecular diagnostic platforms

Next-generation sequencing technologies

Automated immunoassay analyzers

AI-powered laboratory systems

Digital pathology platforms

These technological advancements improve diagnostic accuracy, reduce turnaround time, and enhance laboratory productivity.

Artificial intelligence and automation are increasingly being integrated into diagnostic workflows, enabling faster data analysis and more precise disease detection.

For example, in October 2025, healthcare AI company Eleos introduced Polaris AI, developed in collaboration with Google Cloud. The system utilizes advanced multimodal AI models to analyze behavioral health data and improve clinical decision-making in post-acute care settings. Innovations like these highlight the growing intersection between digital technology and diagnostics.

The presence of leading global diagnostic companies and research institutions across the United States also contributes significantly to rapid innovation in the IVD sector.

Increasing Emphasis on Preventive Healthcare and Personalized Medicine

Preventive healthcare has become a major focus of the US healthcare system. Early detection of diseases can significantly reduce treatment costs and improve patient outcomes.

Diagnostic tests play a central role in preventive healthcare by enabling:

Early disease screening

Risk assessment

Monitoring of chronic conditions

Identification of genetic predispositions

Preventive testing programs for conditions such as cancer, diabetes, and cardiovascular disease have become increasingly common across healthcare systems.

Another major trend shaping the IVD market is the rise of personalized medicine, which uses genetic and molecular data to tailor treatment strategies for individual patients.

Advanced diagnostic tools such as molecular testing, genomic sequencing, and biomarker analysis are essential components of personalized healthcare.

In September 2025, Tempus AI Inc. received 510(k) clearance from the U.S. Food and Drug Administration (FDA) for its RNA-based diagnostic product Tempus xR IVD. The technology is designed to support drug development and precision medicine by providing detailed molecular insights into patient conditions.

The growing demand for personalized treatments will continue to drive innovation and adoption of advanced diagnostic technologies in the United States.

Challenges in the United States IVD Market

Stringent Regulatory Environment

Despite strong growth opportunities, the IVD industry in the United States faces strict regulatory oversight.

Diagnostic products must meet rigorous standards related to:

Clinical validation

Quality control

Safety testing

Post-market monitoring

Obtaining regulatory approval from agencies such as the U.S. Food and Drug Administration (FDA) can be time-consuming and expensive.

For smaller companies and diagnostic startups, navigating complex regulatory requirements can be particularly challenging. These processes often delay the commercialization of innovative diagnostic technologies.

Additionally, regulatory uncertainties surrounding laboratory-developed tests (LDTs) continue to create challenges for diagnostic companies.

Pricing Pressure and Reimbursement Constraints

Another major challenge facing the IVD market is pricing pressure and reimbursement limitations.

Healthcare systems across the United States are increasingly focused on cost containment and value-based care. As a result, reimbursement policies for certain diagnostic tests—especially advanced molecular and genetic diagnostics—can be limited.

Lower reimbursement rates may discourage healthcare providers from adopting expensive diagnostic technologies despite their clinical benefits.

Diagnostic laboratories must balance innovation with financial sustainability, while manufacturers face pressure to maintain profitability in a competitive market environment.

Key Segments of the United States IVD Market

ELISA and CLIA IVD Market

The ELISA (Enzyme-Linked Immunosorbent Assay) and CLIA (Chemiluminescent Immunoassay) segments represent an important portion of the US IVD market.

These immunoassay technologies are widely used for diagnosing infectious diseases, hormone disorders, autoimmune conditions, and cancer biomarkers.

CLIA-based systems are gaining popularity due to their high sensitivity, automation capabilities, and faster test turnaround times. Hospitals and reference laboratories increasingly rely on these systems to process large volumes of diagnostic tests efficiently.

Advancements such as multiplex testing and improved assay performance are further strengthening the demand for ELISA and CLIA diagnostic platforms.

Rapid Test IVD Market

Rapid diagnostic tests have gained significant popularity due to their convenience and ability to deliver quick results.

These tests are widely used in:

Emergency rooms

Clinics

Pharmacies

Home testing environments

Rapid tests are commonly applied for detecting infectious diseases, pregnancy, glucose levels, and cardiac markers.

The COVID-19 pandemic significantly accelerated the adoption of rapid diagnostic technologies, increasing awareness and acceptance of decentralized testing solutions.

Innovations in lateral flow technologies and digital connectivity are improving the accuracy and usability of rapid diagnostic tests, supporting continued growth in this segment.

IVD Reagents Market

Reagents represent a major revenue component of the IVD industry because they are essential consumables used in nearly every diagnostic test.

Laboratories require a continuous supply of reagents for tests across multiple diagnostic categories including:

Clinical chemistry

Molecular diagnostics

Immunoassays

Hematology

High testing volumes for chronic disease monitoring and preventive health screening ensure consistent demand for diagnostic reagents.

Advances in automated analyzers and high-throughput laboratory systems also contribute to increased reagent consumption.

Clinical Chemistry Market

Clinical chemistry remains one of the largest diagnostic segments in the United States.

These tests measure chemical components in blood and body fluids, helping diagnose and monitor diseases such as:

Diabetes

Cardiovascular disorders

Liver diseases

Kidney dysfunction

Common clinical chemistry tests include glucose tests, cholesterol tests, liver function tests, and electrolyte panels.

The growing prevalence of diabetes, obesity, and heart disease continues to drive demand for these routine diagnostic tests.

Automation technologies in clinical laboratories are improving efficiency and enabling laboratories to process larger volumes of samples with greater accuracy.

Microbiology IVD Market

Microbiology diagnostics play a critical role in identifying infectious pathogens and monitoring antimicrobial resistance.

Hospitals, diagnostic laboratories, and public health institutions rely on microbiology testing to detect bacterial, viral, and fungal infections.

Advances in molecular microbiology, automated culture systems, and rapid pathogen identification technologies are significantly improving diagnostic accuracy and speed.

The increasing prevalence of hospital-acquired infections and emerging infectious diseases continues to drive demand for microbiology diagnostics across the United States.

Regional Insights: Key State-Level Markets

Several states contribute significantly to the growth of the US IVD market due to strong healthcare infrastructure and research ecosystems.

California leads the market due to its robust biotechnology industry, advanced research institutions, and innovation hubs such as Silicon Valley and San Diego.

Texas represents another rapidly growing diagnostic market driven by its large population and expanding healthcare infrastructure.

Florida has a high demand for diagnostic services due to its large elderly population requiring regular health monitoring.

Washington plays a major role in the IVD market through strong research institutions and collaborations between technology companies and healthcare organizations.

Together, these states contribute substantially to innovation and adoption of advanced diagnostic technologies.

Major Companies in the United States IVD Market

The competitive landscape of the US IVD market includes several global diagnostic companies driving technological innovation and market expansion.

Key players include:

Roche Diagnostics

Danaher Corporation

Thermo Fisher Scientific Inc.

Bio-Rad Laboratories Inc.

bioMérieux

Abbott Laboratories

Sysmex Corporation

These companies focus on product innovation, strategic partnerships, acquisitions, and research investments to strengthen their market positions.

Final Thoughts

The United States In-Vitro Diagnostics market is expected to experience stable and sustained growth through 2034, supported by the increasing burden of chronic diseases, rapid technological advancements, and the growing importance of preventive healthcare.

As healthcare systems continue shifting toward precision medicine and early disease detection, diagnostic technologies will become even more essential in guiding treatment decisions and improving patient outcomes.

Although regulatory complexities and reimbursement challenges remain key obstacles, ongoing innovation in molecular diagnostics, AI-enabled laboratory systems, and rapid testing technologies will continue to shape the future of the IVD industry.

With strong research capabilities, advanced healthcare infrastructure, and a growing focus on personalized medicine, the United States is likely to remain a global leader in the in-vitro diagnostics market for years to come.

About the Creator

Sakshi Sharma

Content Writer with 7+ years of experience crafting SEO-driven blogs, web copy & research reports. Skilled in creating engaging, audience-focused content across diverse industries.

Keep reading

More stories from Sakshi Sharma and writers in Trader and other communities.

Vegetable Seeds Market Size and Forecast 2026–2034

The global agricultural ecosystem is undergoing a transformative shift as food security, sustainability, and nutritional awareness take center stage. At the heart of this transformation lies the vegetable seeds market — a crucial yet often overlooked segment that forms the foundation of vegetable production worldwide.

By Sakshi Sharma4 days ago in Trader

Mexico Health and Wellness Market Size to Hit USD 81.6 Billion in 2034 | Grow CAGR by 4.53%

Mexico Health and Wellness Market Overview The Mexico health and wellness market is experiencing significant growth as consumers become more conscious of their physical and mental well-being. The market includes a wide range of products and services such as nutritional supplements, organic foods, fitness programs, wellness tourism, and preventive healthcare solutions.

By Jackson Watson3 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.